Complete First Time Buyer Guide

Read time: 10 minsBuying your first home is exciting but it can also be daunting. Everyone wants to share their experience and tell you what to do and what not to do. That is why it is so important to appoint a solicitor who can guide you through each stage of the process, explain the legal jargon, the actions you need to take and be there for advice and support.

Our Guide will take you through every step, from finding a property to collecting your keys and moving in.

We will explain the difference between a freehold and a leasehold property, as well as taking you through some of the complexities of buying a New Build and/or a shared ownership property or a leasehold flat.

Whilst we cannot provide financial advice, our Guide does include a section on the various outgoings involved, so that you can budget accordingly.

If you need to secure a mortgage, you will also find information about when to start the process, how much you might be able to borrow and the different types of mortgages available.

If you haven’t bought a property before you might not fully understand the roles of the various parties involved, including ours as your conveyancing solicitor, so we have included a section on that, as well as the key stages of a purchase transaction.

Before exchange can take place (the point when the transaction is legally binding for all parties) you will need to provide a deposit of at least 5% of the purchase price but more

usually, 10%. Our Guide sets out some of the ways in which your deposit could be funded e.g., a gifted deposit from a parent, or a Help to Buy Isa and how that would work.

Where you are buying with another person you will also want to read about the different methods of ownership, to help you decide which is best for your situation.

You can keep referring to the Guide as your transaction progresses and with the addition of your Kew Law Solicitor, we hope you will feel ready to take your first steps into home ownership.

Make an appointment

"*" indicates required fields

You’re preparing to buy your first home and it starts off exciting. But then the reality sets in. Soon, you’re being bombarded with processes and forms, all in legal speak that you don’t fully understand. You have so many questions: is my property freehold or leasehold? What’s the difference between a licensed conveyancer and a conveyancing solicitor? What are searches? And, the biggest question of all, will I ever make it to completion?

There are a number of stages to navigate before contracts are signed and keys are in hand. That’s why we’ve put together this comprehensive guide, to cut through the confusion and provide you with the answers you need. We cover it all, from finding the right property to exchanging contracts, and everything in between. We’ve even created a handy interactive chart that maps out the entire conveyancing process, so you can see exactly what needs to happen and when. We also talk you through some of the funding support and schemes you may be entitled to as a first-time buyer.

1. Finding Your First Home

- What is Freehold?

- What is Leasehold?

- Properties With a Short Lease

- Shared Ownership Properties

- New Build Properties

You’ve fallen in love with a property and it seems to tick all the right boxes. There’s one factor that you may not have considered and it should be at the top of your list: the form of legal ownership. The two main forms of legal ownership are freehold and leasehold (there are also commonhold properties but these are very rare). These two forms of ownership are extremely different. It’s important to find out which applies to your property before you make any commitments, as it could end up costing you later. You should ask your estate agent to confirm the form of legal ownership as soon as possible.

What is Freehold?

If you own a freehold title to a property, it means you own the building and the land it sits on outright, in perpetuity. You will not have to pay ground rent to a landlord and you will likely be in control of the costs to repair and maintain the property.

What is Leasehold?

If you own a leasehold property then you own a lease to use the property for a number of years. Most leasehold properties will be flats. The lease term can be anywhere between 90 and 999 years. If you are not the original lessee then you will take an assignment of the existing lease on completion of your purchase.

The lease operates as a contract between the freeholder and the lessee and sets down the legal rights and responsibilities of both parties. Often, the freeholder is responsible for the repair, maintenance and insurance of the property while the lessee is required to contribute a proportionate sum towards costs incurred by the freeholder. The lease may also contain restrictions which need to be observed. For example, you may not be allowed pets. You may not be allowed to make any alterations to the property without consent and may be prohibited from sub-letting the property.

Properties With a Short Lease

Where the unexpired lease term (the number of years left on the lease) drops below 80 years, the value of the property can be significantly affected. Lenders require the unexpired lease term to be a certain length. This means that you may be obligated to extend the term of the lease, either when re-mortgaging or selling. The landlord is entitled to charge a premium to extend the lease. Consider the unexpired lease term before making an offer to purchase. You should seek the advice of a chartered surveyor with relevant experience in valuing leasehold property.

New Build Properties

If you are buying a new build property, you may be referred to a conveyancer by a development site office with the promise of speedy service. Your reservation agreement with the developer will likely require you to exchange within 28 days and you may fear losing your reservation fee. However, you should not compromise on the quality of legal advice for the sake of speed. The legal side of buying a new build home is more complex than any other type of conveyancing. That’s because the potential for something to go wrong is much higher with a new build purchase, with issues like non-compliance with planning regulations and incomplete agreements for roads and sewers. These issues can cost you dearly in the future if not addressed. Quite often, referred conveyancers prepare a standard report pack for a development, which is then recycled for every plot they act on. This documentation may not be revisited as the development progresses and new issues arise. The best way to protect yourself is to instruct an experienced conveyancing solicitor to manage the legal aspects of the purchase.

Remember, becoming a homeowner is a legal process, and the law surrounding ownership can be tricky, particularly when it comes to leasehold properties. By engaging an experienced solicitor, with a thorough understanding of the law and conveyancing process, you’ll put yourself in the best position to move forward with your purchase.

Section recap

1. Finding Your First Home

It’s important to find out which applies to your property before you make any commitments, as it could end up costing you later. There are 4 types of property ownership:

- Freehold

- Leasehold

- Shared Ownership Properties

- New Build Properties

Remember, becoming a homeowner is a legal process, and the law surrounding ownership can be tricky, particularly when it comes to leasehold properties. By engaging an experienced solicitor, with a thorough understanding of the law and conveyancing process, you’ll put yourself in the best position to move forward with your purchase.

Action:

You should ask your estate agent to confirm the form of legal ownership as soon as possible.

2. Getting Your Finances Together

- What Should I Budget For?

- Deposit

- Broker Fees

- Mortgage Costs

- Valuation Costs

- Survey Fees

- Legal Fees and Disbursements

- Stamp Duty Land Tax

- Service Charges, Ground Rent and Leasehold Management Costs (If Leasehold)

- Buildings Insurance

- Contents Insurance

- Settling Into Your New Home

Please note we are unable to provide financial advice. We strongly recommend you seek independent financial advice before entering into any financial agreements. Insofar as finances are concerned, this should not be considered advice but more of a note of things you should consider.

What Should I Budget For?

Moving into a new home can be expensive, so it pays to be prepared. You should consider the true cost of moving, so you can budget for those perhaps unexpected costs.

Deposit

Most lenders will ask for a deposit of at least 5%. You should consider managing your savings in the best way possible in order to achieve your savings goal. See our guidance below re Help to Buy ISAs and Lifetime ISAs.

Broker Fees

All brokers take commission from your mortgage provider. Some will charge you a fee for advice, ranging from £300 to £750, and others won’t. A broker will help you compare the market and support you with the process. You do not have to use a broker, but if you do, make sure they are registered to offer mortgage advice by the Financial Conduct Authority. You should also ask whether they’re tied to any specific lender and if they offer advice on mortgages from the whole market. Finally, make sure you’re clear about when any fees need to be paid.

Mortgage Costs

The mortgage you pay for might include a fee. It can either be paid upfront, deducted from the mortgage advance or added to the mortgage balance on completion of your purchase.

Valuation Costs

The lender might arrange a valuation to make sure the property price is realistic. Many lenders don’t charge for this but some do. A valuation should not be confused with a survey. The valuation is for the benefit of the lender only and cannot be relied upon by you. In some cases, your solicitor is prohibited from sharing the contents of the valuation report with you.

Survey Fees

A survey is a report by a qualified professional to highlight any issues that could cost you money to remedy. Surveys range from a basic condition report, which costs around £250 to £300, to a comprehensive building survey, which could cost anywhere between £500 and £2,000, depending on the size of the property. The older or more unusual the property, the more comprehensive the survey should be.

The Royal Institute of Chartered Surveyors can help put you in touch with a qualified surveyor in your area.

Legal Fees and Disbursements

Get an instant quotation for our services by clicking the button below:

Stamp Duty Land Tax

First-time buyers get a discount (relief) that means you’ll pay less or no tax if both of the following apply:

- You, and anyone else you’re buying with, are first-time buyers.

- The purchase price is £500,000 or less.

Where relief is available, the rates of SDLT applicable are: 0% on the first £300,000 of the purchase price, and 5% on the amount above £300,000.

You can see a complete breakdown of the SDLT payable on the government’s website. You can also use their Stamp Duty Calculator.

Service Charges, Ground Rent and Leasehold Management Costs (If Leasehold)

If you are purchasing a leasehold property, you are likely to be liable for ground rent and service charges. If the seller has already paid the ground rent and service charges at the end of the relevant period, you will need to refund the seller for these costs on completion. Ground rents can vary, but are typically between £50-£250 per annum. Service charges can also vary considerably but £1000 per annum is not uncommon. If the seller has paid these annual charges and legal completion takes place towards the beginning of the relevant period, you may have to budget to repay these amounts to your seller on completion. Many landlords and managing agents require the ground rent and/or service charges to be paid to the end of the relevant period on completion in any event, so you may need to pay these to the managing agent on completion, if not the seller.

Buildings Insurance

Your lender will require you to obtain insurance. They will not lend without the insurance being in place. Your buildings cover needs to start on the date you exchange contracts, not the day you move. It is important you arrange this early if you’re buying a freehold property. The freeholder usually arranges this for leasehold properties and will bill you each year. We will be able to confirm this once we have reviewed the lease.

Keep in mind that your policy must cover the cost of rebuilding the property if it is destroyed. This is not the same as the price you pay for the property.

Contents Insurance

This covers loss or damage to your personal possessions, valuables and furniture. The exact level of cover varies by policy, and many providers let you choose cover that suits your needs. It is not compulsory, but contents cover will protect you from costs if something unexpected happens. Some buildings insurance policies for leasehold properties arranged by the freeholder can exclude contents. This cover is quite important where the risk of escape of water (ie flats flooding from above) is fairly high.

Settling Into Your New Home

At the end of it all, you’ll want to have some money left in the bank to make your new home your own. There will be furniture and white goods to buy, and utilities to set up. Do you know how much your council tax will be? You can check with your local authority to see what council tax band your property falls into. There may also be a few added expenses that you hadn’t considered, such as parking permits and unexpected repairs.

Section recap

2. Getting Your Finances Together

These things add up! It’s important to factor all potential expenses in when calculating what home you can afford. If you are worried that your budget won’t stretch far enough, there are a number of affordable home ownership schemes available to first-time buyers including Shared Ownership.

3. Securing a Mortgage

- When Should I Start Applying for a Mortgage?

- What is a Mortgage Agreement in Principle?

- How Much Can I Borrow?

- Fixed and Variable Rate Mortgages

- First-Time Buyer Mortgage Deals

- What is a Guarantor Mortgage?

When Should I Start Applying for a Mortgage?

You should consider making arrangements for your mortgage before searching for your first home. Though it may be tempting to start window shopping for properties, you won’t know what you can afford until you find out how much a mortgage provider is willing to lend. It’s not quite as straightforward as taking the amount you have in savings as deposit. There are a number of factors that a lender will take into account (see below). You don’t want to find yourself in a situation where you’ve set your heart on property, only to have the purchase fall through as you can’t borrow as much as you expected. By starting the process early and obtaining an agreed mortgage in principle, you can avoid lengthy delays and disappointments.

What is a Mortgage Agreement in Principle?

Though you won’t complete the full mortgage process until you’ve had an offer accepted on a property, all lenders will be able to give you a preliminary indication of what they are prepared to lend. Some mortgage providers will offer you a mortgage agreement in principle. As a buyer, this provides proof of your borrowing power and may put you at an advantage over competing buyers. Mortgage providers offer a mortgage agreement in principle as an incentive for you to select them as a lender (though there is no obligation for you to do so). Your mortgage in principle is based on a series of initial credit checks and you will need to provide evidence that you meet their eligibility criteria. Before requesting a mortgage in principle, you should compare the market to ensure you are getting the best possible deal.

How Much Can I Borrow?

There are three main factors that lenders take into account when determining how much you can afford to borrow:

Salary

Lenders will typically lend 4 to 4.5 times your salary. They will also take any other income outside of your main salary into account, such as investments.

Outgoings

Lenders will conduct a thorough assessment of your monthly outgoings to determine how much of your mortgage you’re able to repay. This will include estimates of your monthly spending, bills, and loans, as well as the number of dependents (ie children) that you support.

Credit History

Lenders will perform a series of credit checks to determine the risk involved in offering you a a loan. Any previous debts, arrears, or bankruptcy will be flagged and will impact your chances of obtaining a mortgage. Lenders will also stress test your finances to ensure you’re able to maintain repayments if your personal circumstances change, for example if you have a baby or become seriously ill.

Fixed and Variable Rate Mortgages

When selecting a mortgage, you need to decide where you want a variable or fixed rate of interest. With a fixed rate, your repayments won’t be affected by any changes to interest rates. Lenders will fix your rate for a set period, usually between two and five years, but sometimes longer. This option is popular with first-time buyers as it offers certainty over your monthly payments, and you won’t be impacted by any fluctuations in the market. However, with a fixed rate mortgage, you will be liable to pay a penalty known as Early Repayment Charge if you leave your mortgage before the agreed term. Also, unlike variable rate mortgages, your payments won’t go down if interest rates drop.

First-Time Buyer Mortgage Deals

You may also be entitled to special deals and mortgage rates as a first-time buyer. Usually these incentives are designed to alleviate the initial expense of buying your first home. First-time buyer mortgages may include a lower deposit, reduced application fees, and a cheaper rate for the first few years. You should be wary of any incentives that end up costing you considerably more in the long run.

What is a Guarantor Mortgage?

Guarantor mortgages are mortgages designed for first-time buyers who are receiving financial support from a guardian or relative. A guarantor will agree to pay for your mortgage if you are unable to make a repayment. Having a guarantor alleviates the risk to the lender, meaning they are more likely to approve your application. An alternative option is the Barclay’s Family Springboard Mortgage. Here, there are options for a guarantor, or ‘helper’, to cover the full cost of the deposit. This will be held in a designated savings account with the lender and released after a fixed period if the mortgage payments are maintained.

4. Your Deposit

How Much Deposit Do I Need?

Most banks will ask you to pay at least 5%, and more often 10%, of the value of the property for a deposit. However, it’s always a good idea to save as much as you can in advance. This obviously reduces the amount that you will have to pay back in the long term and also gives you a much wider choice of cheaper mortgage products in the short term. According to Halifax, the average deposit first-time buyers paid in 2021 was almost £59,000. This is why so many first-time buyers look for financial help, often in the form of gifted deposits from family members, to help boost their savings and get a step on the property ladder.

The Bank of Mum and Dad

If you are receiving a gift to help with the purchase of your first home there are some things you’ll need to consider to ensure your application can progress smoothly.

- The estate agent will likely want to see evidence of the source of funds to comply with various money laundering legislation. The donor should be prepared to part with their bank statements and ID documentation.

- A standard instruction from lenders to conveyancers is to report where funds are being used towards a transaction that did not originate with the borrower/purchaser. To avoid delay, you must disclose the gifted element of your deposit to your broker and/or lender at the outset of your mortgage application.

Help to Buy ISA

You can no longer open a Help to Buy ISA. If you already have a Help to Buy ISA, you can continue paying in up to £200 each month until November 2029. The government will top up your savings by 25% (up to £3,000) when you buy your first home. If you are buying with someone who also has a Help to Buy ISA, both of you will receive the 25% bonus. You can claim the 25% bonus until November 2030.

Example

Lenders will typically lend 4 to 4.5 times your salary. They will also take any other income outside of your main salary into account, such as investments.

| Your savings | Government payment | Total |

|---|---|---|

| £1,600 (minimum) | £400 | £2,000 |

| £4,000 | £1,000 | £5,000 |

| £12,000 (maximum) | £3,000 | £15,000 |

The home you buy must:

- have a purchase price of up to £250,000 (or up to £450,000 in London)

- be the only home you own

- be where you intend to live

As your solicitor, we will apply for the extra 25% during the conveyancing process which will be paid to us before legal completion. The bonus must be used towards the purchase price of the property. Just make sure you let us know you are using a Help to Buy ISA so that we can process the appropriate declarations and closing statements in time to claim the bonus. You cannot make use of the bonus post-completion of your purchase. Any bonus funds received after completion will need to be returned to the government.

Lifetime ISA

You can use a Lifetime ISA (Individual Savings Account) to buy your first home. You must be 18 or over but under 40 to open a Lifetime ISA. You can put in up to £4,000 each year, until you turn 50. You must make your first payment into your ISA before you’re 40.

The government will add a 25% bonus to your savings, up to a maximum of £1,000 per year. The Lifetime ISA limit of £4,000 counts towards your annual ISA limit which is £20,000 for the 2021 to 2022 tax year.

To open and continue to pay into a Lifetime ISA you must be a resident in the UK, unless you’re a crown servant (for example, in the diplomatic service), their spouse or civil partner.

You can withdraw money from your ISA if you’re buying your first home. If you withdraw cash or assets for any other reason, you’ll pay a withdrawal charge of 25%. This is known as making an unauthorised withdrawal. This recovers the government bonus you received on your original savings.

You can use your ISA to help you buy your first home if all the following criteria apply:

- the property costs £450,000 or less

- you buy the property at least 12 months after you make your first payment into the

- Lifetime ISA

- you use a conveyancer or solicitor to act for you in the purchase (the ISA provider will

- pay the funds directly to them)

- you’re buying with a mortgage

If the person you’re buying with has a Lifetime ISA, they can also use their savings and government bonus.

They’ll pay a 25% withdrawal charge to use their Lifetime ISA savings if they own or have a legal interest in another property (for example they’re a beneficiary of a trust that includes property).

If you have a Lifetime ISA and a Help to Buy ISA, you can only use the government bonus from one of them to buy your first home.

You can transfer money from a Help to Buy ISA to a Lifetime ISA. However, if you transfer money from a Lifetime ISA to a Help to Buy ISA, you’ll have to pay the 25% withdrawal charge.

Unsecured Loans

It is essential to flag any unsecured borrowing you are intending to finance your deposit with to your broker and/or lender at the outset. Many lenders will not agree to additional borrowing. You will have to provide evidence of source of funds. If a loan is disclosed at a late in the process, you could find yourself liable for any costs if the lender withdraws your mortgage offer.

5. Closing the Deal

- Subject to Contract

- The Role of Your Conveyancing Solicitor

- The Role of the Estate Agent

- The Role of a Surveyor – ‘Caveat Emptor’

- Why Do Searches?

- Investigation of Title

- Raising Enquiries

- Reviewing, Approving and Exchanging Contracts

- Insuring Your Property

- Paying Relevant Taxes

This is the part where we come in! Buying a home is a legal transaction as well as a financial one. Conveyancing is the legal process by which the title of a property is transferred. In this section, we outline the role your conveyancing solicitor will play, and show you the key touchpoints of the conveyancing process through to completion.

Subject to Contract

You have had your offer to purchase accepted but it remains subject to contract. There is no binding agreement for the sale until exchange of contracts (see the conveyancing process below). Each party reserves the right to withdraw until a binding contract is made. There is no recourse to the seller and you must be prepared to accept any incurred costs if the transaction does not proceed to exchange.

The Role of Your Conveyancing Solicitor

A conveyancing solicitor delivers support and guidance throughout the conveyancing process. Most importantly, we provide you with relevant legal advice in language that you’ll understand. To offer the best possible service, your conveyancer needs to have an in-depth understanding of the intricacies of land law, as well as a thorough knowledge of the formation and formalities of contracts, misrepresentation, and remedies for breach of contract. A conveyancing solicitor will have undertaken extensive legal study and continued professional development in these areas. As solicitors are a regulated body, you’ll receive a high quality service you can trust. The firms in which they operate also maintain professional indemnity insurance.

If you are buying a new build property, you may be referred to a conveyancer by a development site office with the promise of speedy service. Your reservation agreement with the developer will likely require you to exchange within 28 days and you may fear losing your reservation fee. However, you should not compromise on the quality of legal advice for the sake of speed. The legal side of buying a new build home is more complex than any other type of conveyancing. That’s because the potential for something to go wrong is much higher with a new build purchase, with issues like non-compliance with planning regulations and incomplete agreements for roads and sewers. These issues can cost you dearly in the future if not addressed. Quite often, referred conveyancers prepare a standard report pack for a development, which is then recycled for every plot they act on. This documentation may not be revisited as the development progresses and new issues arise. The best way to protect yourself is to instruct an experienced conveyancing solicitor to manage the legal aspects of the purchase.

The Role of the Estate Agent

The estate agent’s role goes beyond simply marketing and selling your home. They communicate with the many parties involved to ensure that everyone is working towards the common goal of legal completion. The agent identifies issues up and down the chain and can provide you with the necessary information to manage expectations in terms of timescales etc. Too often a scenario arises where you are ready to exchange but are prevented by unknown obstacles down the chain. Your conveyancing solicitor is limited in what they can do and will only receive information from the seller’s solicitor. The estate agent can get to the source of a problem quickly.

The Role of a Surveyor – ‘Caveat Emptor’

Caveat emptor (‘let the buyer beware’) is a cornerstone of conveyancing in England and Wales. The law imposes a clear obligation on you as a buyer to find out about a property, as it only recognises a limited duty of disclosure from the seller. It is therefore essential to find out as much as possible about a property before contracts are exchanged, as you will have to take the property in whatever condition when there is a binding contract for the purchase. You should consider instructing a chartered surveyor to provide a survey report to highlight any matters of concern or consideration before you commit to exchange.

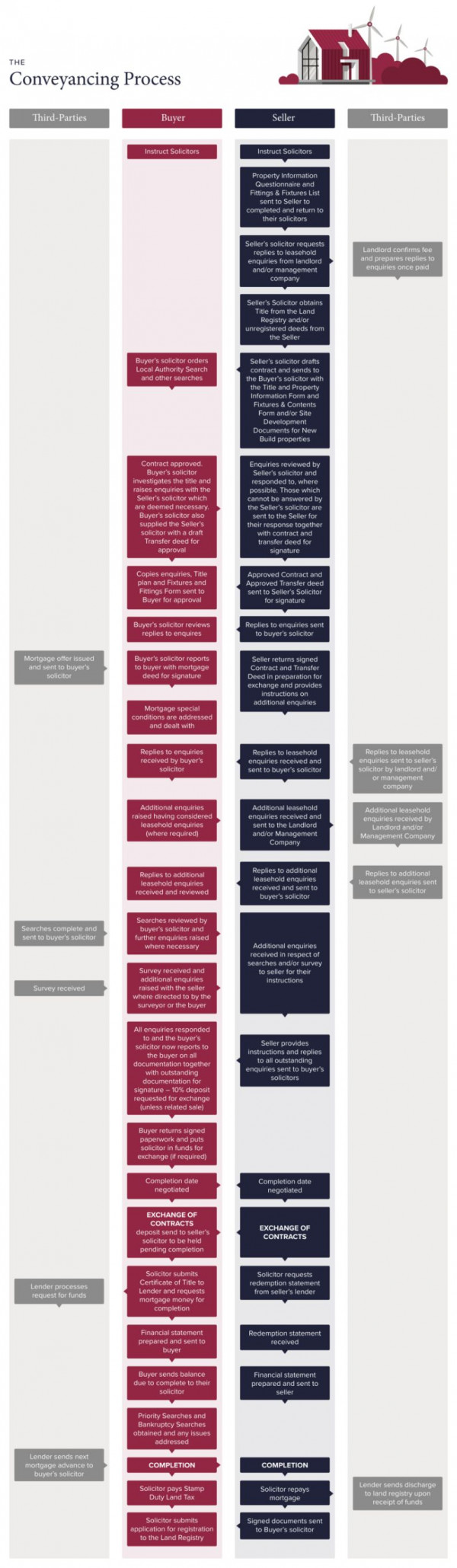

THE

Conveyancing Process

Third-Parties

Buyer

Seller

Third-Parties

Instruct Solicitors

Property Information Questionnaire and Fittings & Fixtures List sent to Seller to completed and return to their solicitors

Seller’s solicitor requests replies to leasehold enquiries from landlord and/or management company

Landlord confirms fee and prepares replies to enquiries once paid

Seller’s Solicitor obtains Title from the Land Registry and/or unregistered deeds from the Seller

Buyer’s solicitor orders Local Authority Search and other searches

Seller’s solicitor drafts contract and sends to the Buyer’s solicitor with the Title and Property Information Form and Fixtures & Contents Form and/or Site Development Documents for New Build properties

Contract approved. Buyer’s solicitor investigates the title and raises enquiries with the Seller’s solicitor which are deemed necessary. Buyer’s solicitor also supplied the Seller’s solicitor with a draft Transfer deed for approval

Enquiries reviewed by Seller’s solicitor and responded to, where possible. Those which cannot be answered by the Seller’s solicitor are sent to the Seller for their response together with contract and transfer deed for signature

Buyer’s solicitor reviews replies to enquires

Replies to enquiries sent to buyer’s solicitor

Mortgage special conditions are addressed and dealt with

Replies to enquiries received by buyer’s solicitor

Replies to leasehold enquiries received and sent to buyer’s solicitor

Replies to leasehold enquiries sent to seller’s solicitor by landlord and/or management company

Additional enquiries raised having considered leasehold enquiries (where required)

Additional leasehold enquiries received and sent to the Landlord and/or Management Company

Additional leasehold enquiries received by Landlord and/or Management Company

Replies to additional leasehold enquiries received and reviewed

Replies to additional leasehold enquiries received and sent to buyer’s solicitor

Replies to additional leasehold enquiries sent to seller’s solicitor

Searches complete and sent to buyer’s solicitor

Searches reviewed by buyer’s solicitor and further enquiries raised where necessary

Additional enquiries received in respect of searches and/or survey to seller for their instructions

Survey received

Survey received and additional enquiries raised with the seller where directed to by the surveyor or the buyer

All enquiries responded to and the buyer’s solicitor now reports to the buyer on all documentation together with outstanding documentation for signature – 10% deposit requested for exchange (unless related sale)

Seller provides instructions and replies to all outstanding enquiries sent to buyer’s solicitors

Buyer returns signed paperwork and puts solicitor in funds for exchange (if required)

Completion date negotiated

Completion date negotiated

EXCHANGE OF CONTRACTS

deposit send to seller’s solicitor to be held pending completion

EXCHANGE OF CONTRACTS

Lender processes request for funds

Solicitor submits Certificate of Title to Lender and requests mortgage money for completion

Solicitor requests redemption statement from seller’s lender

Financial statement prepared and sent to buyer

Redemption statement received

Buyer sends balance due to complete to their solicitor

Financial statement prepared and sent to seller

Priority Searches and Bankruptcy Searches obtained and any issues addressed

Lender sends next mortgage advance to buyer’s solicitor

COMPLETION

COMPLETION

Solicitor pays Stamp Duty Land Tax

Solicitor repays mortgage

Lender sends discharge to land registry upon receipt of funds

Solicitor submits application for registration to the Land Registry

Signed documents sent to Buyer’s solicitor

Why Do Searches?

We always recommend undertaking a Local Authority Search, a Water Search and Environmental Search when you buy a home. These will be conducted when you obtain your mortgage.

- Commons Registration Search

- Coal Mining search

- Index Map search

- Land Charges search

- Company Search

- Other searches dependent upon the location of the property

You can find an example of the Local Search, Drainage Search and Environmental Search here.

Investigation of Title

Your solicitor will investigate the evidence of title produced by the seller’s solicitor and will raise enquiries (requisitions) on any matters that are unsatisfactory or unclear. It is likely that your solicitor will also act for your lender. The lender will ensure there are no defects in the title which would adversely affect the lender’s ability to sell the property and recover the loan. Your solicitor will ensure that title is good, marketable, and free from incumbrances that will adversely affect the use and enjoyment of the property. Where your solicitor also acts for the lender, they will ensure the title conforms with the mortgagee’s instructions to the solicitor.

Raising Enquiries

Many conveyancers still practise defensive lawyering and issue as many enquiries as possible. This heavy-handed approach is sadly not uncommon and can lead to unnecessary delays. Our solicitors only raise necessary and specific enquiries, ensuring that you receive focussed advice when we report to you on the title.

Reviewing, Approving and Exchanging Contracts

We consider the terms of the draft contract scrupulously in the light of your instructions, the replies to pre-contract enquiries, the results of the searches, and the title investigation. If amendments to the contract are necessary then we’ll make the amendments and send to the seller’s solicitor for approval. You need to sign the contract before exchange. It is standard conveyancing practice to have two identical contracts, one signed by the seller and the other signed by the buyer. These are exchanged so that the buyer receives the seller’s signed contract, and the seller receives the buyer’s signed contract.

Insuring Your Property

As soon as there is a valid contract, the beneficial ownership in the property passes to you. This means that you bear the risk of any loss or damage to the property, subject to the seller’s duty to look after the property. In addition, the contract is likely to pass the risk to the buyer on exchange (unless the contract is for a purchase of a new build property where the risk is likely to remain with the developer). It is obviously important for a buyer to arrange adequate insurance of the property from the moment of exchange because if the property is damaged (e.g., by fire), the buyer will still be contractually bound to complete the purchase.

Paying Relevant Taxes

Once completion has taken place we shall prepare and submit online your SDLT return as your agent, and pay the tax due (if any). We will ensure (if you are eligible) that we make an application for First-Time Buyer Relief.

More information about First-Time Buyer Relief can be found here: https://www.gov.uk/government/publications/stamp-duty-land-tax-relief-for-first-time-buyers-guidance-note

6. Methods of Ownership

- Registering Your Ownership

- Co-Ownership

- Joint Tenants

- Tenants in Common

- Declaration of Trust

- Deciding on the Right Method of Ownership

Registering Your Ownership

Once we are in receipt of the signed Transfer from the seller’s solicitor, we will make an electronic application to register your purchase at the Land Registry. The Land Registry receives around 18,000 requests to change the register per day so it is unlikely that the register will be updated with your details immediately. Most changes are completed within a month of the Land Registry receiving the application. Applications to register Transfers of Part (most New Build properties, for instance) are likely to take in excess of 6 months.

Co-Ownership

If you are buying the property with another person, you will become a co-owner. As co-owners, you can hold the property in one of two ways:

- As joint tenants;

- As tenants in common.

“Joint tenants” and “tenants in common” are ways of describing how you own the property. The terms have different legal meanings to tenants who rent property from a landlord.

Joint Tenants

If you hold the property as joint tenants, both of you will own the whole of the property. You will not each have a quantified share in the property and will not be able to leave a share of the property in your will.

If you sell the property, or if you separate, it will be presumed that you own the property equally, regardless of your respective contributions to the purchase price. If one co-owner dies, their interest in the property will automatically pass to the remaining co-owner without any further action. The surviving co-owner will own all of the property and, upon their death, it will form part of their estate. This is known as the “right of survivorship”.

Married couples, or those in a civil partnership, commonly use this method of co-ownership because the right of survivorship makes it straightforward to inherit each other’s shares in the property.

However, there may be reasons not to become joint tenants. For example, if one of you has made a larger contribution to the purchase price of the property and you would want this to be recognised if the property is sold or if you separate. A joint tenancy is also not suitable if you have a family from an earlier marriage and wish to leave your interest in the property to them, instead of passing it to the other co-owner.

Tenants in Common

If you hold the property as tenants in common, each of you will own a specified share in the property. You need to consider whether each person’s share will be fixed from the outset or whether the shares will vary according to the financial contributions made by each person.

If you opt for fixed shares, your shares may be equal, but they do not have to be. Holding the property as tenants in common in unequal shares may be desirable if you have made unequal contributions to the purchase price of the property.

If your shares are fixed, you need to decide the size of those shares now. You may need to revisit the split later down the line to reflect any relevant changes in circumstance. For example, if one of the co-owners pays the costs of significant improvements to the property.

If your financial contributions towards the property throughout your ownership are unequal (for example, if one person pays a larger proportion of the mortgage repayments), you may want your shares to reflect this.These calculations will be more complex and you will need to keep accurate records of each person’s contributions.

As tenants in common, your share of the property can be passed on to another person, either during your lifetime or under your will. If you do not have a will at the time of your death, then your share will pass in accordance with the rules of intestacy. Holding the property as tenants in common may be appropriate if you have children from previous relationships and would prefer them to inherit your interest on your death rather than your co-owner.

Declaration of Trust

If you wish to hold the property as tenants in common, you should sign a declaration of trust. A declaration of trust is a document that formally records that you hold the property as tenants in common and sets out your respective shares in the property. If you sell the property, or if you separate, the declaration of trust will be referred to in order to determine your entitlement to the sale proceeds from the property.

Deciding on the Right Method of Ownership

How you wish to hold the property must be your own decision and is something that you should keep under review following the purchase of your property. If you decide to hold the property as joint tenants but then wish to split your interests, you can “sever” the joint tenancy and turn it into a tenancy in common at any time. It is also possible for tenants in common to become joint tenants at a later date by entering into a new declaration of trust.

You should be aware that if you decide to hold the property as joint tenants:

- Either party can sever the joint tenancy without the other’s agreement.

- The joint tenancy may be severed automatically in various situations, including where one party becomes bankrupt.

- You will need to take out a suitable life insurance policy to cover the mortgage if one of you dies before it is paid.

- You should make a will, or review your existing will, to ensure property passes in accordance with your wishes (this is particularly important if you hold as tenants in common at the time of death).

It is important to specify and document how you wish to hold the property now, to avoid any uncertainty or future litigation.

You’ve Got This!

We know this all seems very daunting. Buying a home is a huge commitment- financially, legally, and emotionally. As a first-time buyer, it’s important to feel informed and empowered so that you can ask the right questions and make the best decisions for your situation.

We hope this guide has alleviated the stress of the unknown and helped you take this important step with confidence. Your conveyancing solicitor will be there to guide you throughout the process and answer any questions you have.

Frequently Asked Questions

When should I instruct a conveyancer?

Ideally as soon as your offer is accepted. The earlier you instruct, the quicker the legal work can start (e.g., ID checks, initial forms, contract request from the seller’s solicitor).

What is a property search and why do I need it?

Searches are investigations carried out by your conveyancer to uncover issues that could affect the property or your ability to use it. Common searches include:

· Local Authority search

· Water & Drainage search

· Environmental search

Your mortgage lender will always require these. Other searches may also be necessary depending on the location e.g., a Mining Search.

What is exchange of contracts?

This is when the transaction becomes legally binding. You will:

· pay your deposit

· fix a completion date

· commit to buying the property

After exchange, pulling out would result in financial penalties.

What is completion?

This is the day you legally become the owner. Funds are transferred to the seller’s solicitor, and you receive the keys.

Do I need a survey as well as conveyancing?

Yes, a survey assesses the physical condition of the property. Conveyancing assesses the legal status. They complement each other.

Examples

Example A

Missing Building Regulations Certificate

James is buying a 1930s terraced house; the seller had added an extension but could not provide a Building Regulations Completion Certificate. James asked his surveyor to check that there were no structural issues with or caused by the extension. Once this had been confirmed, James’ conveyancer negotiated a building regulations indemnity insurance to satisfy the lender and the sale proceeded without delay.

Example B

Guidance for first time buyer with a Help to Buy Isa

Sally is a first-time buyer, and she will be using £4,000 from savings in a Help to Buy Isa. Sally is aware that she will receive a bonus from the government, but she doesn’t understand how this gets paid to her and what actions she needs to take. Sally speaks to her solicitor at Kew Law for some advice. They explain that once the transaction is a little closer to exchange, they will ask her to close her HTB Isa Account, provide them with the Closing Statement and sign a declaration confirming that she is a first-time buyer. Kew Law will then use these documents to claim the bonus from the government, which will be paid directly to them and not to Sally. Sally is grateful for the advice and is delighted that she can continue to pay into the HTB Isa for now, as she wants to try and increase the amount of bonus payable.

Ready to take the next step?

Get in touch with a member of our conveyancing team.

Book your Initial Consultation

0800 987 8156

Fiona Parsons

Partner

Lauren Beech

Solicitor

Maddi Luck

Licensed Conveyancer

Emma Donovan

Partner

Ryan Pound

Senior Associate (Solicitor)

Harriet Hovell

Solicitor

Michelle Delieu

Licensed Conveyancer

Thomas Grove

Solicitor

Connie King

Senior Associate (Solicitor)

James Kew

Managing Partner

William Brown

Senior Associate (Solicitor)

Mandy Mapes

Conveyancer